Market Insights

When hiking in the Swiss Alps last year from Chamonix to Zermatt, I found myself faced with difficult sections of the mountain to cross. Fortunately, security was provided by chains, ropes and ladders for these more challenging areas. Whilst I can plan my routes to avoid these spots entirely, I can also rationalise that this security significantly decreases the danger, even so, not everyone will simply discard their fears or worries.

Similarly, Central Banks have been providing a form of security or ‘safety’ to reduce our fears, but unlike the physical presence of the chains placed on the mountains, their monetary actions appear not to have provided sufficient safety to stimulate wide corporate investment and economic activity, nor to raise inflation rate expectations in the real economy.

Despite the lack of those broader economic benefits, the expansionary monetary policy and stubbornly low inflation expectations have successfully inflated asset prices, making those who have been invested richer during the process. In this respect, Central Banks have provided sufficient security.

Clearly, geopolitics and the potential threat of a pandemic health event have the power to change risk perception. In this vain, the Coronavirus has clearly already impacted markets this year. With interest rates already extremely low, a large reduction to economic growth expectations could quickly change investors’ perception of the safety and support that Central Banks are able to provide.

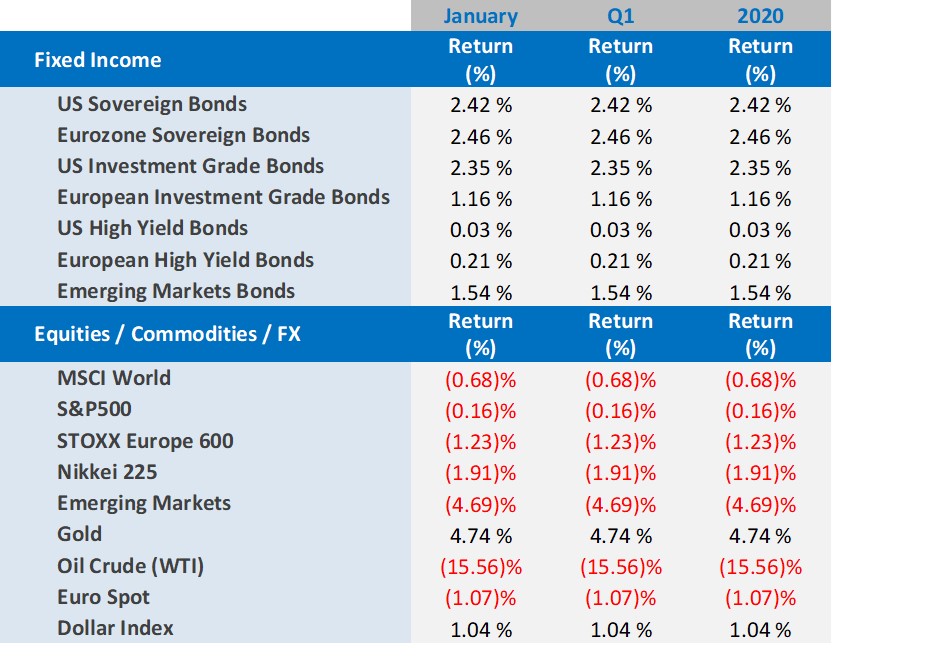

- Developed market equities: Initial fears of an escalation of events between the US and Iran pushed equity markets lower, only for them to recoup their losses before increasing fears around the Coronavirus outbreak and its potential negative impact on the market later in the month. The S&P500 lost 0.16% in the United States, the STOXX Europe 600 lost 1.23% and in Japan, the Nikkei 225 lost 1.91%.

- Fixed income markets gained during the month, with safe haven assets clearly outperforming as ‘lower for longer’ interest rate expectations were additionally supported by growing fears that the Coronavirus would negatively affect growth. US Treasuries gained 2.42%, US investment grade bonds gained 2.35% and US high yield bonds gained 0.03%. In Europe, sovereign bonds gained 2.46% and investment grade bonds gained 1.16%, while European high yield bonds gained 0.21%.

- Emerging markets were driven by fears over the Coronavirus outbreak, with equities and fixed income markets following a similar global pattern. EM equities lost 4.69%, while EM bonds gained 1.54%.

- Oil moved with the industrial commodity complex and lost considerable ground due to the strong linkage with Chinese consumption, losing 15.56%.

- Gold gained 4.74%, climbing initially on geopolitical worries and broadly holding close to its recent new highs.

Global markets in numbers

Market Outlook and V3´s position

Difficult as it is to make macro-economic and asset class return forecasts in more normal times, the Coronavirus and its unknown future path (and therefore potential to alter the current economic growth and inflation expectations) clearly contributes to an already complicated mix.

With the information we do have, and despite the newspaper column inches dedicated to significant health worries, we feel that global growth will be only modestly lower for the first two quarters. This should pick up again as containment and the approaching Northern Hemisphere summer help to reduce the virus’s impact, however we continue to monitor the situation as it develops.

You may be wondering, what about the US election scheduled for late this year, President Trump’s tweets, further potential US trade frictions with various trading partners and the UK’s exit from the European Union at the end of the year? Whilst important, we believe these events should not drive markets in the first half of 2020.

Therefore, we should concentrate on the outlook for growth, inflation and likely Central Bank actions. The IMF (International Monetary Fund) published its latest World Economic Outlook in January, which points to modest/sluggish growth and inflation remaining low (annual growth of 1.6% and annual inflation < 2.0% in the Advanced Economies in 2020 and 2021). Central Banks should remain in their current mode of action, with markets pricing additional rate cut/s from the US Federal Reserve.

Corporate profits should broadly grow and, even if growth is relatively low, better corporate earnings and dividends should support equity markets. We do not expect returns to even closely match last year, but still look for positive returns.

Fixed Income markets delivered such strong returns in 2019, thanks to support from narrowing spreads and rallying government bonds. This year it seems that, even with yield hungry investors continuing to be net buyers, probably the only support Fixed Income markets are likely to receive is from lower US rates across the yield curve.

Should we see lower US interest rates later in the year this could assist in weakening the USD, which in turn would likely support gold prices and the broader commodity complex.

In summary, we believe that a combination of the perception of security offered by the current level of Central Bank support; low but positive economic growth; and a lack of inflation alarm bells, should support investors’ risk appetite. This appetite will ultimately be the principal guide, although it is often our perception of risk that drives our choices, and, as always, maintaining a diversified portfolio can assist in reducing overall portfolio risk.

So what will your 2020 look like? Chains or a change of route altogether?

For more information, please contact our Chief Investment Officer, Tom Milner, on:

+41 22 715 0910

tom.milner@v3cap.com

Cover image: Shutterstock