Market insights

Have you ever had the feeling that you have already lived an exact moment? Promnesia, or déjà vu, as it is more commonly known, affects 70% of the world’s population. I have certainly felt that ‘wow, I’ve lived this before’ sensation countless times throughout my life. Investors, analysts and anyone with half an eye on the global markets will have experienced it, with some apprehension, after what happened last month.

The uncanny similarity between the performance of equity markets in January 2018 and January 2019 makes one wonder whether they will also replicate the same patterns over the rest of the year. Last year, impressive gains in the first month propelled the S&P500 to its highest level in history in an unstoppable rally that wowed investors already wary about the length of the bull market and its future. We all know how that played out…the following month the bull market hit a wall, bringing with it the first fears of a market correction, which happened not once, but twice in 2018. Obviously, should something similar happen this year, that would be nothing more than a coincidence, but with several analysts still calling for a market contraction before the end of the quarter, it would probably be the longest collective déjà vu in the history of mankind! What a feat!

Let’s have a look at what actually did happen in January this year: Broadly speaking, equity markets enjoyed an amazing ride, ending up with steep gains across the board in both developed and emerging markets. Fixed income markets also had strong gains, with commodities following suit. It was a sea of gains in the markets and here is how it played out:

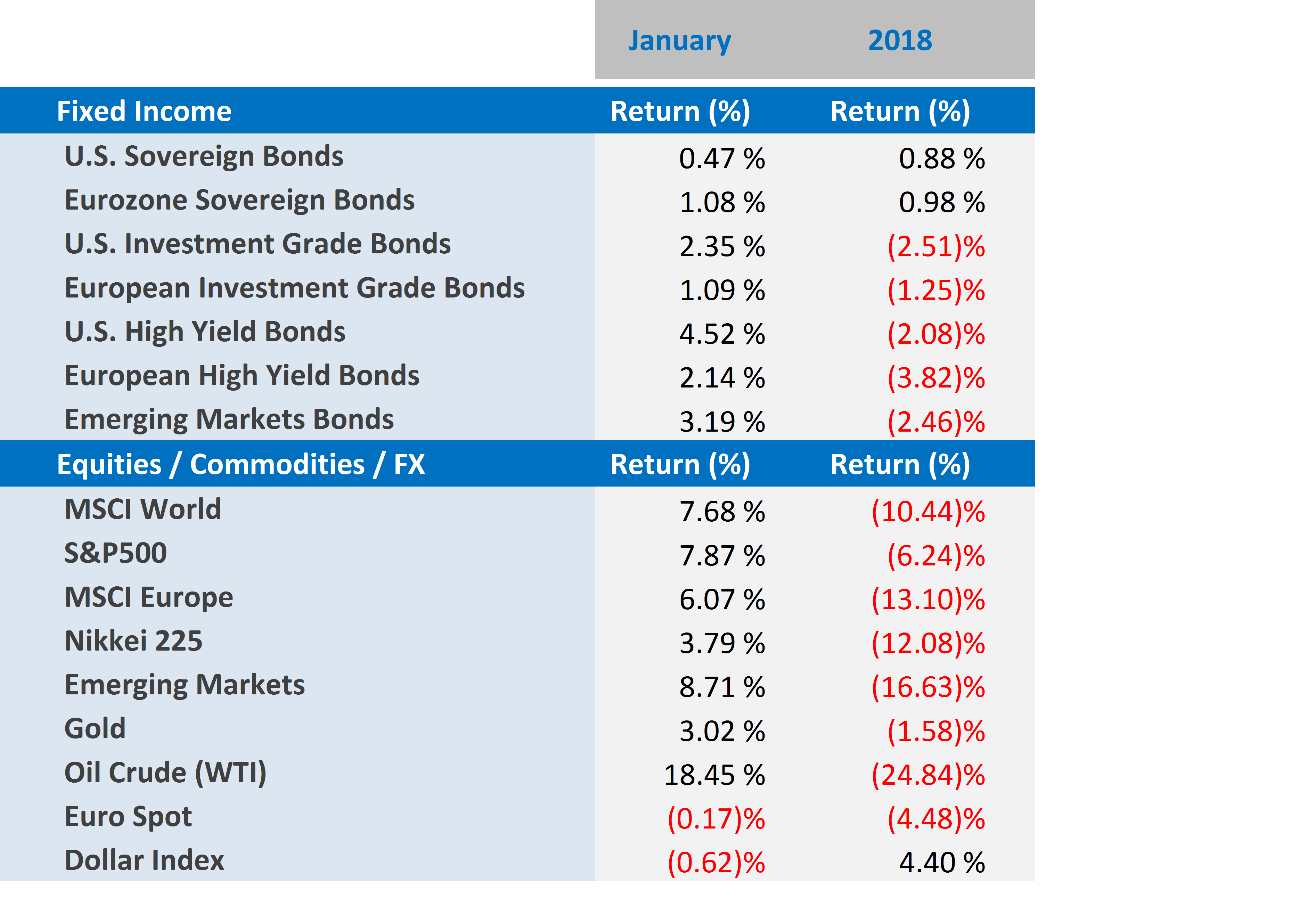

- Developed market equities had their strongest January since 2012, as strong corporate earnings results and an upbeat sentiment surrounding the US-China trade talks kept investors optimistic. This was intensified by the US Federal Reserve commenting that it was pausing its interest rate hike cycle in January and becoming more dependent on economic momentum. As a result, the global market rout from the previous month was mostly reversed, led by the US. At the end of the month, the S&P500 gained 8.97% in the United States, the MSCI Europe gained 6.07% and in Japan, the Nikkei 225 gained 3.79%.

- Fixed income markets had a strong month, with the support and blessing of the Federal Reserve in the US, which suggested it would be patient and refrain from increasing interest rates in the US unless conditions were right. Credit markets strongly outperformed safe havens both in the US and Europe, as investors took advantage of the high probability that interest rates peaked in the US last December. US Treasuries gained 0.47%, US investment grade bonds gained 2.35% and US high yield bonds ended the month up 4.52%. In Europe, sovereign bonds gained 1.08%, investment grade bonds gained 1.09% and European high yield bonds gained 2.14%.

- Emerging markets enjoyed gains across the board, helped by the strong risk-on sentiment in the markets and by the weaker US Dollar. EM equities jumped 8.71%, and EM bonds gained 3.19%.

- Oil recovered part of its losses of the previous months, jumping by 18.45% in January alone, its sharpest gain on record for the month. Prices were driven up as a result of output cuts by OPEC and Russia (which took effect on January 1st), optimism related to US-China relations and US sanctions on Venezuelan owned PDVSA. That being said, the commodity is still trading 29% below its October 2018 high.

- Gold had another strong month, gaining 3.02% in January, as investors welcomed the weaker dollar. The physical demand for the yellow metal is expected to increase, as central banks continue to add to their reserves.

Global markets in numbers

Market Outlook and V3´s position

It can be challenging to focus on the future when we feel that we are re-living the past. Our natural tendency to chase comfort and find that in known patterns, means that there is a risk that investor behaviour will be a repeat of 2018. In other words, this year, we may see a replay of the bullish trend from the beginning of last year, followed by losses in February, March, October and above all, December.

Although the Federal Reserve took a huge weight off the markets by announcing that it would not automatically increase interest rates and shrink its balance sheet, instead relying on economic momentum to decide its next steps, unfortunately other risks are far from subdued.

A quick romp through the biggest and most threatening: Number one has to be the US-China trade war: despite the positive sentiment generated by (mostly Chinese) officials making an effort to publicly show discussions are moving forward, we cannot ignore the negative impact that the US investigation on Huawei will likely have – by way of reminder, Huawei has been accused of being involved in numerous cases of intellectual property theft from US companies, as well as selling US technology to sanctioned countries, such as Iran. Other major risks include Brexit (will it happen?), Italy and its huge debt burden, the possibility of a conflict in Venezuela with an US-led coalition force pounding against Russia and China’s interests in the country and increasing geopolitical temperature across the globe.

Whilst you could argue that the trade talks and the Huawei investigation are not interconnected, as one is political and being lead by the White House and the other criminal and therefore headed by the Department of Justice, it would be naïve to imagine that they will not be discussed in tandem over closed doors between officials of both countries. It is not difficult to imagine that we may have another déjà vu with Trump praising his Chinese counterpart to the press, just to tweet minutes later that the US must act to deter and tame Chinese ambitions, throwing markets in an unwarranted swing from optimism to bitter pessimism in a matter of seconds.

All of which serves to reinforce why it is so important to always ensure portfolios are well balanced and take risk into consideration. But, how can we structure our portfolios to cope with all that? As I have mentioned before, it is time to take advantage of the current market strength to perform a portfolio check, making sure that it is both aligned with investors’ long-term goals, as well as taking into consideration the short-term risks surrounding us currently.

At V3, for now we are not altering our neutral stance in equities nor our positive view in emerging market bonds. We believe that these two asset classes will be the main source of positive performance for portfolios in 2019 and are confident that, even if some of the risks mentioned before do materialise, there is value in staying selectively invested in those markets. Sound familiar? Don’t worry, this time it is not déjà vu. It is just a pure and simple repetition of our mantra. After all, when something makes sense you stick to it, even if it has been done before.

For more information, please contact our Chief Investment Officer, Cássio H. Valdujo, on:

+41 22 715 0910

cassio.valdujo@v3cap.com

Cover image: https://www.shutterstock.com/image-illustration/two-poles-twisted-clock-face-time-112763704